Watchdog Comments on Ethics Commission Regs for Outside Activity Approvals

VIA EMAIL

Michael Sande

Commission on Ethics and Lobbying in Government

25 Beaver Street, New York, NY 10004

Re: Plain language for outside activity regulations is useful, but real estate compensation approvals should not be limited

Dear Mr. Sande,

We write to provide comments on the Commission on Ethics and Lobbying in Government’s (COELIG) proposed amendments to Part 932, “Outside Activity Restrictions and Approval Procedures,” as published in the May 20, 2026 New York State Register.

We support your goal of providing more plain language and clarifying the approval process for statewide officials for outside activity. While we find it surprising that statewide officials would need greater clarity on the approval process for outside activities, the new language more directly describes the process to be followed.

However, we caution that the amendments that define business ventures related to real estate as those that are incorporated could limit the types of outside activities that are subject to approvals.

Business Ventures and Real Estate Income

The amendments in Part 932.2 Definitions adds “Business Venture,” and provides the following definition for it (emphasis added in bold):

“(c) Business Venture means any activity, other than Employment, engaged in by an individual subject to this Part, either individually or as part of a group, which is intended to achieve financial gain. For purposes of this Part, ownership of investment or rental real property (other than one’s primary or secondary home) shall constitute a Business Venture if the property is held by a limited liability corporation or other corporate entity.”

In other words, in the context of real estate holdings, business ventures would only be those where the property is owned by a limited liability company or another corporate entity. While it does not say “including but not limited to,” we note that the next definition regarding compensation eliminates “whether or not incorporated,” in reference to business ventures (emphasis added in bold):

([c]d) Compensation [shall] means the financial consideration received in exchange for services rendered, e.g., wages, salaries, benefits, professional fees, royalties, bonuses, or commissions on sales. Compensation shall also include income received from any [b]Business [v]Venture[, whether or not incorporated,] that is owned or controlled, in whole or in part, by an individual who is subject to this Part. Notwithstanding the foregoing, income received from transactions involving such individual’s own securities, personal property, or [real estate] primary or secondary residence is not included in the term Compensation.

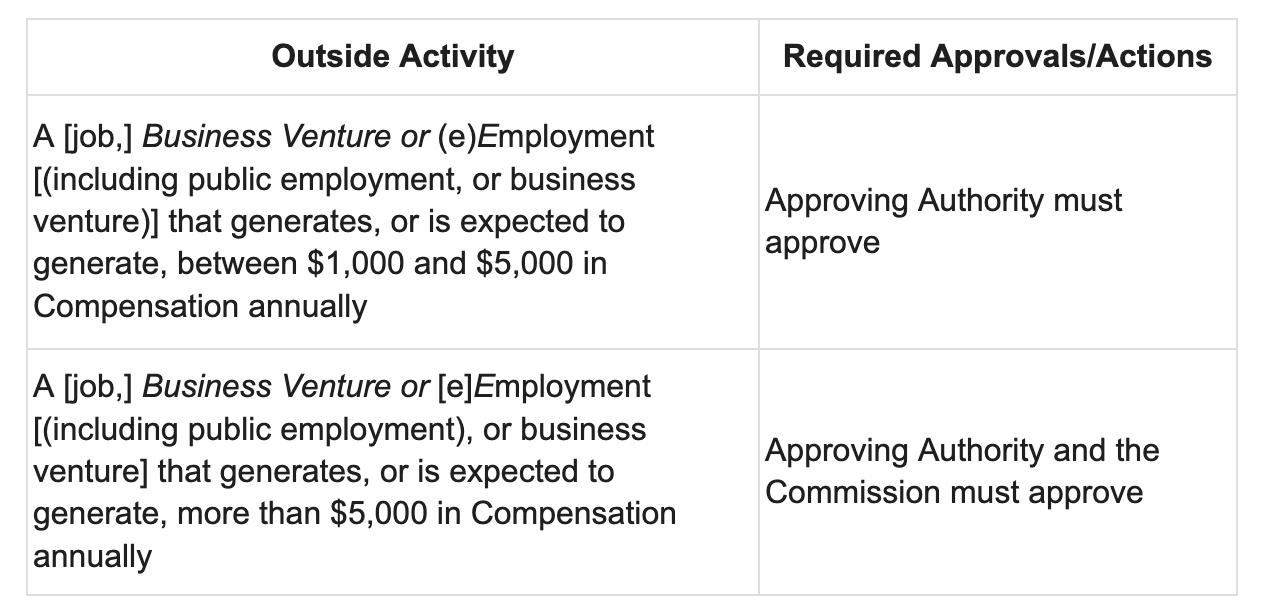

In Section 932.5: Required Prior Approval for Salaried Policymakers, Heads of State Agencies, and Statewide Elected Officials, the chart that summarizes required approvals is also amended to insert business ventures and delete “job” as follows:

Taken together, it appears that COELIG is limiting the required approval for outside activity related to real estate holdings to only those held by an LLC or another incorporated entity.

It is our understanding that financial disclosure statements would capture income of $1,000 or more from all real estate transactions or earnings of the policymaker, whether or not they are held by business ventures that are LLCs or other incorporated entities. Therefore it appears that there could be reportable income from real estate that is not subject to outside activity approvals.

We urge COELIG to ensure that all real estate income over $1,000 is subject to outside activity approvals, regardless of whether it is held by an LLC or other incorporated entity. This would be consistent with the outside income that is reported on financial disclosure statements. While this would capture more activity and result in more approvals, it is better to err on the side of being overinclusive. There could be scenarios in which policymakers deliberately do not set up LLCs or incorporate their real estate holdings in order to evade the approval process.

The definition of compensation already excludes income related to real estate transactions involving one’s primary or secondary residence, so we cannot see the harm in ensuring that all other real estate earnings are subject to approvals.

Thank you for your consideration.

Sincerely,

Rachael Fauss

Senior Policy Advisor

Reinvent Albany

cc. Members of the Commission on Ethics and Lobbying in Government